On July 17, 2025, the Ethiopian Federal Parliament approved the Income Tax Amendment Proclamation No. 1395/2025 (“Amendment Proclamation”), which revised the existing Income Tax Proclamation No. 979/2016. (“Income Tax Proclamation”). The Amendment Proclamation has taken effect as of July 7, 2025. The new law forms part of the Ethiopian government’s broader effort to modernise the tax system, expand the tax base, and raise the contribution of tax and customs revenues to 11% of the GDP. The Amendment Proclamation introduces new tax rates and brackets, as well as new rules for tax collection. These changes introduce significant compliance obligations for businesses operating in or engaging with Ethiopia. Below, we set out a summary of the key changes.

Revision of Permanent Establishment Rules

Under the Income Tax Proclamation, a permanent establishment is created when there is a fixed place of business where the business is wholly or partly conducted. The designation of a permanent establishment is relevant in determining whether an income is Ethiopian source income, the taxation of certain payments made to non-residents, the transfer pricing rules and withholding obligations of taxpayers. The Amendment Proclamation has reduced the threshold for creating a permanent establishment from the current 183 days (within six months) to 91 days within 12 months. This will have implications for non-residents for income generated in and from Ethiopia.

Expansion of Ethiopian Source Income

The Amendment Proclamation expands the definitional scope of “Ethiopian-Sourced income” to capture tax revenue from the rapidly evolving landscape of e-commerce and digital content creation. Beyond what is provided in the Income Tax Proclamation, income earned by non-residents from transmitting information in Ethiopia—via cable, radio, optical fibre, television broadcast, VSAT, internet satellite, or similar means—will be deemed Ethiopian-source income, regardless of the origin of the information. This means that income generated from these services will be taxed in Ethiopia. By broadening the tax net to cover income streams from modern information transmission and digital services, the new law aims to ensure its tax system keeps pace with technological advancements.

Introduction of Minimum Alternative Tax

The Amendment Proclamation introduces the concept of Minimum Alternative Tax (MAT). The MAT system requires taxpayers to pay tax at a rate of 2.5% if the income tax calculated on their total business income is below 2.5% of the annual turnover. Payments made under the MAT regime are creditable against future income tax liabilities for up to five years. The MAT also applies to companies enjoying income tax exemptions under relevant investment incentives laws. In such cases, the MAT is calculated based on the income tax payable after applying the tax incentives. Given that companies that benefit from tax incentives are exempt from paying corporate income tax for a certain period under the current Investment Incentive Regulation, the practical impact of this introduction will become clear over time. The MAT system aims to capture revenue from loss-declaring taxpayers over multiple years by compelling them to contribute a minimum tax, which will be credited against future profits.

Changes to Taxpayer Categorisation

The existing three taxpayer categories is now reduced to two under the Amendment Proclamation:

- Category A: Entities and individuals with an annual gross income of ETB 2 million or more.

- Category B: Individuals with annual income below ETB 2 million. Entities such as companies, state-owned enterprises, and other bodies—whether established in Ethiopia or abroad—that are required to maintain books of account are excluded from this definition.

Following this categorisation, the Amendment Proclamation now requires Category B taxpayers to be taxed based on annual gross sales, rather than based on net profit under a standard assessment system. Moreover, the new law requires Category B taxpayers to maintain books of account and Category A taxpayers engaged in multiple business activities to keep separate books of account for each activity.

Introduction of an Advance Income Tax Payment System

Previously, taxpayers were required to pay business income tax at the end of the tax year. The Amendment Proclamation introduces an advance income tax payment system. Both Category A and B taxpayers must now make quarterly advance payments equal to 25% of the prior year’s tax. Category A taxpayers are required to make this payment within 5 days of each quarter’s end, while Category B taxpayers must make the payment within 15 days of each quarter. New taxpayers are exempt for the first year of operations. If the annual income tax liability is less than the total amount paid through quarterly instalments, the excess will be refunded to the taxpayer. If it is higher, the taxpayer must pay the difference at the end of the year.

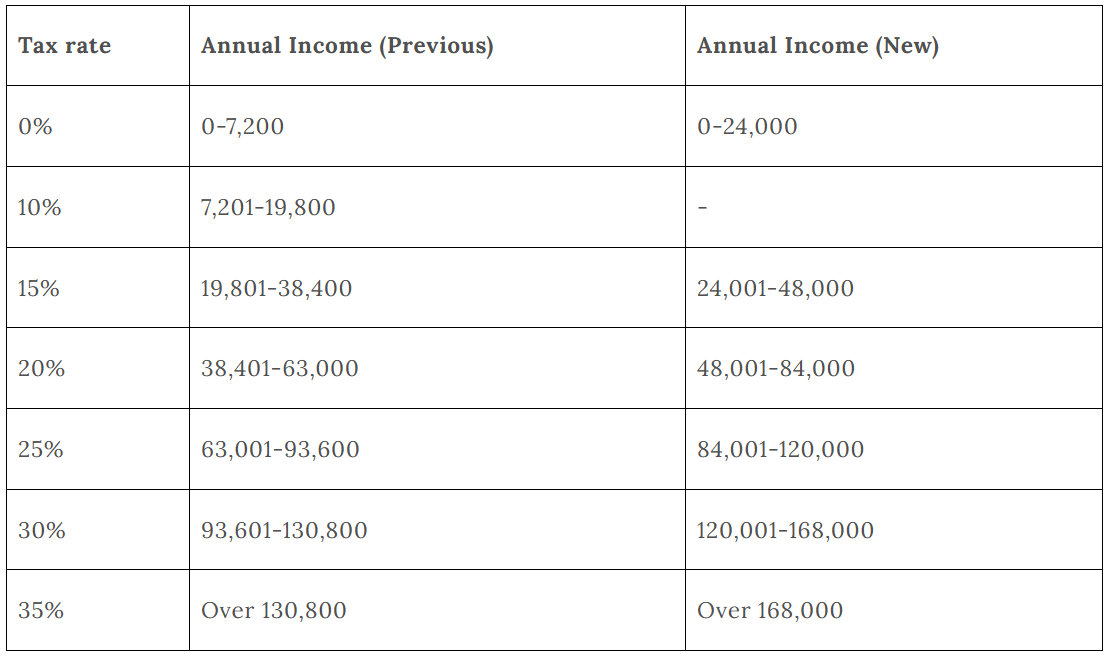

Revised Tax Brackets

The Amendment Proclamation adjusted employment income tax brackets and other brackets that apply to rental, and individual business income. Below are the changes:

The table below provides the revised income tax rate from rental and business income for individuals:

It is worth noting here that no changes have been made to corporate income tax, which stands at 30%.

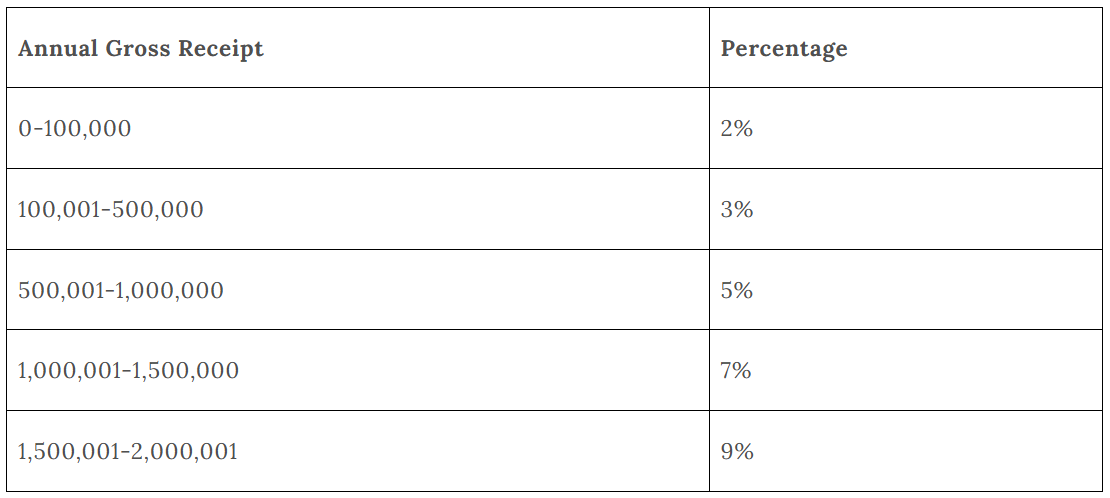

Elimination of Presumptive business taxes

The Amendment Proclamation eliminated the presumptive business taxes that were previously applied. Now Category B taxpayers are required to pay tax on annual gross sales at the following tax rates:

This tax rate will not be applicable on the following categories, even if their income falls under Category B:

- Professional services which include accounting, architectural, consulting, construction, engineering, financial economy, and investment professional, healthcare, and legal. These professions are required to maintain books of accounts and will be taxed at ordinary corporate income tax at a rate of 30%

- VAT-registered business, and

- Businesses opting for net income taxation under Schedule C of the Income Tax Proclamation (i.e., 30% for corporate income tax or 0% - 35% for individual businesses)

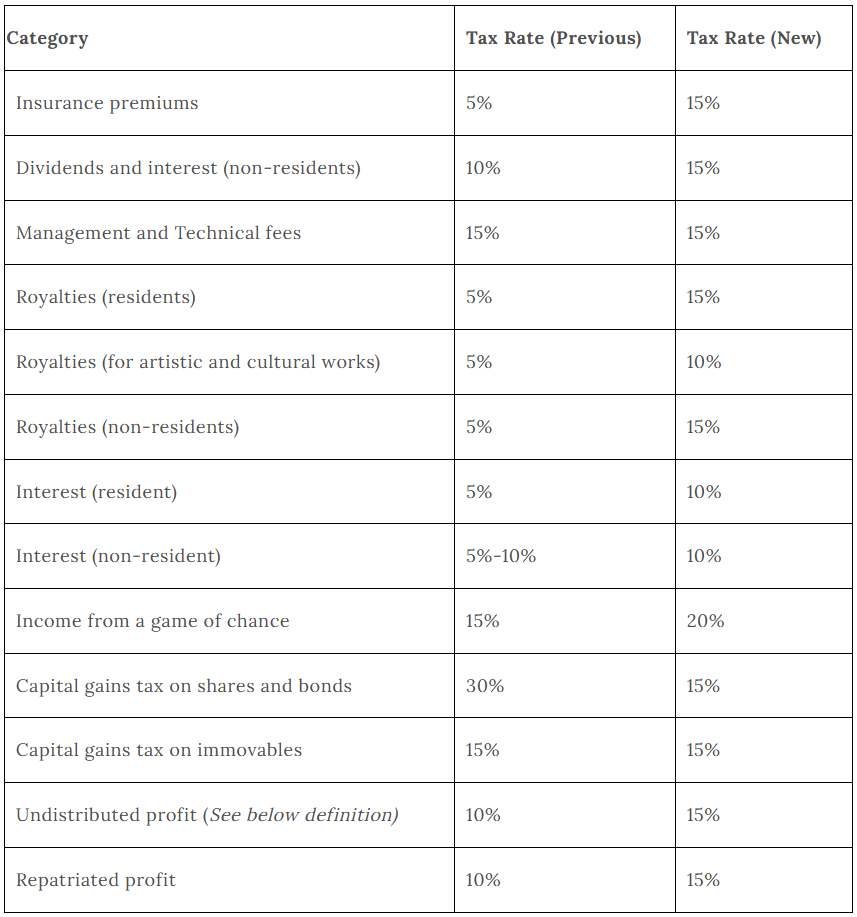

Changes to Withholding Tax Rates

The Amendment Proclamation made the following adjustments to withholding tax rates for resident and non-resident taxpayers:

In addition, withholding tax on local payments for goods and services is raised from 2% to 3% for the supply of goods involving more than Birr 20,000 in one transaction or supply contract and the supply of services involving Birr 10,000 in one supply contract.

Clarification on Undistributed Profit

The Amendment Proclamation defines undistributed profit as net profit that:

- Are not distributed to shareholders

- Are not reinvested to increase the company’s capital or the shares of the shareholders within one year

- Or are not remitted to a foreign company operating through a permanent establishment in Ethiopia.

Further, the new legislation provides that the extent of tax exemption for a dividend payment used to settle subscribed shares will be specified in a future directive.

Introduction of Pass-through Tax Treatment

The Amendment Proclamation introduced a pass-through tax treatment for limited liability partnerships (LLPs) and registered collective investment funds. These entities are exempt from corporate income tax. Instead, tax will only apply to partners based on the income tax threshold and to investors as dividend tax. LLPs typically used by professionals such as lawyers and auditors will benefit from this new provision. Details on the accounting of expenses of LLPs are expected to be governed by future directives. Concerning collective investment schemes, the Ethiopian Capital Market Authority is expected to issue a directive on the establishment and operation of and further details on the taxation will be outlined in a forthcoming tax regulation.

Exempt Income Additions

The Amendment Proclamation introduces new categories that will be exempted from tax:

- Premiums from newly issued shares by existing companies. (Previously, premiums were subject to capital gains tax.)

- Dividends paid to resident companies holding at least 12.5% directly or indirectly the voting rights and have control in the distributing company

Enhanced Oversight of Foreign Employees

The Amendment Proclamation introduces a new obligation on government bodies with a view to tracing and implementing taxes on expatriate employees. The Ethiopian Investment Commission and the Ministry of Labour and Skills are now required to notify the tax authority when issuing or renewing work permits to expatriates. Further, the new law requires cooperation between the Ministry of Revenue and the Ministry of Foreign Affairs for information sharing on the employment income of employees working for foreign embassies in Ethiopia and international organisations.

Digital Content Creators Brought into the Tax Net

Digital content creators, who earn income on a consistent and professional basis, are now subject to income tax. Income from digital content creation will be taxed either as business income (0 to 35%) or under Schedule “D” as other income at 15%. Income from digital content creation will be taxed as business income if it is conducted regularly for profit, in a professional or organised manner, or involves maintaining records or incurring business expenses. If these conditions are not met, the income will be taxed as "Other Income" under Schedule D at a 15% rate. Classification of digital content creation as a business activity based on factors such as income level, transaction type, content type, and business purpose will be determined in a future directive. Platforms are also required to report the annual income of content creators.

The Amendment Proclamation also introduced the concept of digital services, a service that involves digital content. A detailed definition of digital services and the corresponding income tax rate, which will not exceed 5%, will be provided in a future regulation. At this stage, it is not clear who will be covered under this provision.

Elimination of Turnover Tax (TOT)

The Amendment Proclamation repeals the existing turnover tax (TOT) regime. Previously, taxpayers with annual transactions below 2 million Birr were required to register and collect TOT at a rate of 10% on taxable supplies of goods or services. While the Amendment Proclamation seeks to eliminate TOT entirely, it does not clarify the implications for existing taxpayers—whether they will transition to the VAT system or be exempt from collecting the tax altogether.

Payment Restrictions for Traceability

The Amendment Proclamation restricts cash transactions. Payments to taxpayers must now be made through approved channels such as bank transfers or cheques. Cash payments are limited to ETB 50,000 per day. Violations will trigger administrative penalties. This requirement will not apply to public bodies, public enterprises, banks, microfinances or other entities which the Ministry of Finance will provide through a directive.

Uniform Income Tax Exemption

The Amendment repealed all income tax incentives granted except those granted to investments under the Investment Incentives Regulations and Cooperative Proclamation for cooperatives.

Conclusion

The Amendment Proclamation introduces changes that will impact businesses. The expanded taxation of non-residents, particularly through the revised permanent establishment rules and the broader definition of Ethiopian-source income, extends Ethiopia’s taxing rights to a wider range of cross-border transactions, including digital services and information transmission.

Further, the shift to quarterly advance tax payments is a consequential measure that will likely have a notable impact on how companies plan and manage their cash flows. Without an efficient refund and credit system from the tax authority, this measure could place considerable strain on liquidity.

Equally notable is the reduction of the capital gains tax from 30% to 15%, along with the exemption of collective investment schemes from corporate income tax. These are positive measures that will likely encourage greater investment in the capital market. However, the increase in the dividend tax rate from 10% to 15% may deter some investors from participating in the equity market, potentially pushing them to explore alternative investment options.

While the Amendment introduces sweeping reforms, many practical aspects—such as the treatment of digital services, taxation of collective investment schemes, accounting for professional services, and scope of exemptions for dividend payments - will depend on detailed directives still to be issued.

For more information, contact: Eskedar Ezezew: eskedar@mekdesmezgebu.com

--

Read the original publication at Mekdes & Associates